Belgian companies face a challenge that almost no other country in Europe shares: they must communicate their ESG story not in one language, but in three. Most handle this as a translation problem. It is not. It is a communication problem — and the difference is costing them credibility with exactly the audiences they are trying to reach.

What ESG communication actually means

ESG communication is the process by which a company explains its environmental, social, and governance commitments to external stakeholders — investors, regulators, journalists, clients, and the general public. It is distinct from ESG reporting, which is a compliance exercise. Communication is about trust. Reporting is about data.

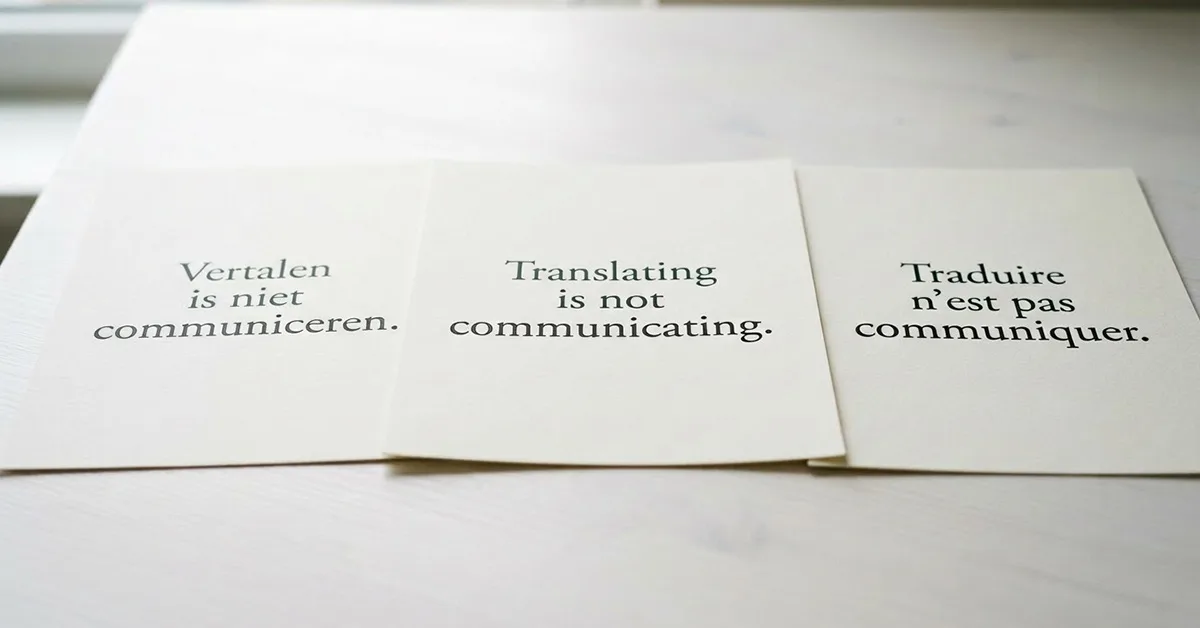

The distinction matters in Belgium because the two are routinely conflated. Companies produce a CSRD-compliant sustainability report in Dutch, translate it mechanically into French and English, and call it ESG communication. They have produced three documents. They have communicated nothing.

Effective ESG communication requires that each stakeholder group — in each language community — receives a message calibrated to what they care about, in language that reads as native, not translated. In Belgium, that means understanding that Flemish business press treats ESG very differently from francophone financial media. It means knowing that an English-language investor deck for a Luxembourg fund audience has different expectations than one prepared for a London analyst. The words may be the same. The framing cannot be.

Why Belgium’s multilingual structure makes this harder than it looks

Belgium is one of three countries in the European Union with three official languages and three distinct media landscapes. A sustainability story that lands well in De Tijd will need substantial rethinking before it is pitched to L’Echo — not because the facts change, but because the editorial culture, the terminology, and the implicit assumptions of the readership are different.

This is not a minor stylistic consideration. Research on ESG communication effectiveness consistently shows that perceived authenticity is the primary driver of stakeholder trust — and authenticity erodes instantly when readers detect that a text was written for someone else. A French-speaking CFO reading a Dutch original that has been translated rather than written will know within two paragraphs. The same applies to the institutional investor reading a sustainability report that was conceived in Dutch and retrofitted into English.

The CSRD changes the stakes. Since Belgium transposed the EU Corporate Sustainability Reporting Directive in 2024, large Belgian companies face mandatory non-financial reporting with assured data. The 2026 Omnibus revision raised the employee threshold to 1,000, postponing obligations for many mid-sized companies to 2028 — but the voluntary reporting trend is moving faster than regulation. According to ESG Dive, nearly 90% of European companies now excluded from mandatory CSRD scope still plan to maintain or expand their sustainability reporting. They are doing it for competitive and reputational reasons, not because they must.

That means the companies voluntarily communicating on ESG are the ones who want to be seen as leaders. Getting the communication wrong is a bigger reputational risk for them than for companies that report only because they have to.

The three mistakes Belgian companies make most often

Mistake one: treating translation as localisation. The most common failure. A sustainability report is written in Dutch, handed to a translation agency, and the output is declared the French and English version. The result reads like a translation — correct, but inert. The ESG claims that felt grounded and specific in Dutch become generic in French. The narrative that felt confident in Dutch feels bureaucratic in English. Stakeholders in each language community read something that was clearly not written for them.

Mistake two: one message for all audiences. Institutional investors, retail shareholders, NGOs, regulators, journalists, and employees all read ESG communication with different questions in mind. An investor wants to understand material risk. A journalist wants a story. A regulator wants compliance evidence. An employee wants to know whether the commitments are real. Companies that publish a single sustainability report and point all audiences to it are answering none of these questions well. Corporate financial communications — the discipline that structures financial and non-financial information for specific audiences — exists precisely to solve this problem. A well-structured approach to corporate financial communications disaggregates the message and delivers each version to the audience that needs it.

Mistake three: confusing ambition with credibility. The single fastest way to lose ESG credibility is to state ambitions that are not grounded in specific, verifiable commitments. Unverifiable ESG claims escalate quickly from a communications problem into a reputational crisis. Belgian stakeholders — particularly in the Flemish business community, which has a high tolerance for directness — read ESG language carefully for vagueness. Phrases like “committed to reducing our impact” or “working toward a more sustainable future” have become so common as to mean nothing. The companies that earn trust are the ones that say: we reduced Scope 1 emissions by 14% in 2025, here is the methodology, here is the assurance provider. Specificity is not a compliance requirement. It is a communication choice.

What good ESG communication looks like in practice

The companies communicating ESG effectively in Belgium share three characteristics.

They write each language version as an original, not a translation. The Dutch version is written by someone who thinks in Dutch and understands the Flemish business press. The French version is written by someone who knows how francophone financial media works. The English version is written for the international audience that will actually read it — typically investors and analysts who are not native speakers themselves, and who therefore value clarity above elegance.

They segment their audiences before they write a word. Investor-facing communication, employee-facing communication, media-facing communication, and regulatory-facing communication are treated as separate briefs. Each has a different primary message, a different level of technical detail, and a different tone. The same discipline that applies to financial PR and investor relations applies here — the audience determines the message, not the other way around.

They treat ESG communication as an ongoing discipline, not an annual exercise. A sustainability report published once a year and never referenced again creates a credibility gap. Companies that integrate ESG messaging into their quarterly communications, their press releases, their CEO positioning and executive speeches, and their client conversations build a consistent signal that stakeholders can verify over time.

The CSRD communication opportunity most companies are missing

The revision of the CSRD in early 2026 created an unexpected opportunity for companies that are communicating voluntarily. With many mid-sized Belgian companies now technically excluded from mandatory reporting until 2028, the companies that continue to report — and communicate — on their ESG commitments will stand out from peers who retreat to silence.

This is a significant competitive differentiation window. In markets where sustainability credentials influence procurement decisions, investment allocation, and employer brand, being the company that communicates clearly while others go quiet is a position worth occupying.

The window will not stay open. As reporting obligations extend further down the company size spectrum, voluntary ESG communication will become the baseline expectation. The companies building that communication infrastructure now — in three languages, for multiple audiences, with verifiable specificity — are building an asset that compounds over time.

Frequently asked questions

Does ESG communication in Belgium need to be in all three national languages?

There is no legal requirement for ESG communication (as distinct from statutory reporting) to be in all three languages. However, companies with stakeholders in both language communities — which includes most mid-to-large Belgian businesses — face a practical credibility gap if their sustainability messaging is only available in one language. For investor-facing communication, English is typically required regardless of the company’s domestic language.

What is the difference between a sustainability report and ESG communication?

A sustainability report is a structured document that meets regulatory or voluntary reporting standards — ESRS, GRI, or similar frameworks. ESG communication is the broader practice of building stakeholder understanding and trust around a company’s environmental, social, and governance commitments. The report is an input to communication, not the communication itself.

How does the CSRD revision of 2026 affect Belgian companies?

The 2026 Omnibus revision raised the employee threshold for mandatory CSRD reporting to 1,000 employees, postponing obligations for many mid-sized Belgian companies to 2028. However, the revision does not change the voluntary reporting landscape — companies below the threshold that have been communicating on ESG are not required to stop, and many are choosing to continue for competitive and reputational reasons.

What makes ESG greenwashing a legal risk in Belgium?

The EU’s Green Claims Directive, which Belgium will implement in line with EU timelines, prohibits unsubstantiated environmental claims in commercial communication. This creates legal exposure for companies that make broad ESG claims — in any language — without the supporting data to back them. The practical implication: every ESG claim in public communication should be traceable to a verifiable data point or commitment.

How should a Belgian company approach ESG communication for international investors?

International investor communication on ESG should be in English and structured around the frameworks investors use to evaluate ESG risk — primarily TCFD for climate, and the disclosure categories investors will recognise from ESRS or GRI. The Belgian context — including the multilingual operating environment, the Belgian corporate governance code, and the specific regulatory timeline under the transposed CSRD — should be explained explicitly, as many international investors have limited familiarity with it.